No matter how well we plan, everyone has to manage risk - in good times and in bad. Building risk management into your day-to-day planning will benefit you greatly when things don't go as expected.

1. Track your risks and issues

This may sound obvious, but many professionals fail to track and manage risks in any meaningful way. With our focus normally on delivery and problem-solving, we often don't spend enough time thinking about potential risks to our projects. Equally, by not considering uncertainties we can also be caught flat-footed when an opportunity arises that we can't capitalise on.

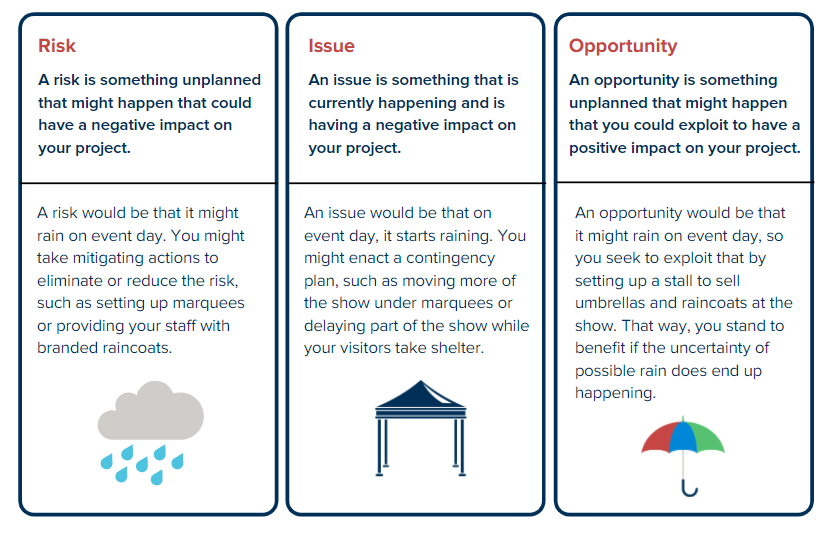

2. Know the difference between a risk, an issue and an opportunity

We hope you enjoyed our fuller article on this earlier in the white paper, so we won't dwell on this again here!

3. Get the basics in order

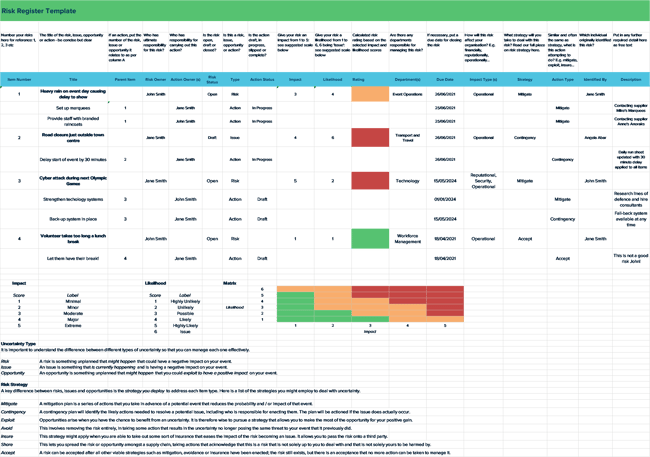

An effective risk management framework needs two key components: a risk management approach, and a risk register.

It is important to define who in your organisation is responsible for recording, managing and reporting on risks, who is responsible for making decisions on risk, and who is responsible for carrying out the actions. For larger organisations, these roles can vary depending on the severity of the risk being managed: some risks need to be dealt with right at the very top.

So how do you categorise risk? A good risk approach should set guidelines for impact and likelihood scales so that classification is consistent across all risks. For financial risks, as an example, it makes sense to set thresholds for each impact level based on the overall project budget. A financial impact of £0-£1,000 could be classified as 1, whereas a financial impact of £100,000+ could be a 5, with appropriate thresholds in between.

4. Record your risks effectively

Being clear and concise when you record your risks goes a long way to ensuring you manage them effectively. All risk registers will have a place to capture a title and description as minimum. Make sure you include the basics of uncertainty, event, and outcome in your title to make it clear what the risk or opportunity is.

An example of a poor risk capture might be 'heavy rain'. This title does not tell us anything about the potential issues this might cause. Instead, be more descriptive, with something like 'possibility of heavy rain, leading to local flooding, resulting in the course becoming unusable'. Anyone reviewing the risk register will know exactly what the risk is at a glance, with more detail going into the description.

It's also important to only capture the risks that may have a material impact on your project. Don't waste time discussing and resolving risks that would have little to no impact if they were to come to pass.

5. Plan your steps, and act on them

Once you have identified your risks, you need to act on them. See our earlier article on risk strategy for the possible steps you could take here. It's important to be open-minded about the different ways that you could approach an uncertainty.

6. Uncertainty is not just about risk, it's also about opportunity

Again, we hope this message has become clear throughout the start of this white paper. There is a tendency in risk planning to only focus on preventing negative outcomes, but uncertainties can also create positive possibilities - but only if we are ready to act when an opportunity arises.

7. Be open, transparent and accepting about risk

This attitude is vital. Risk management is about looking into the future and planning for uncertainties. It is not about apportioning blame where planning has not been up to scratch. The identification of risks is important to project management and should be encouraged by all levels of management. No project or event, big or small, can ever go 100% to plan.

By regularly looking at your risk profile and assessing where gaps may exist, you will improve the overall delivery of your work and be better prepared when issues do occur. By building strategic responses, the ability of your organisation to respond will be strengthened. You won't be able to plan for every eventuality - but you will be able to better respond by putting your plans into action.

Not every field will be useful to every risk manager, but each provides valuable information in tracking uncertainty. The key is to be consistent so that you and anyone else managing risk for your organisation or event can understand all of the information in the risk register.

Not every field will be useful to every risk manager, but each provides valuable information in tracking uncertainty. The key is to be consistent so that you and anyone else managing risk for your organisation or event can understand all of the information in the risk register.